Thank you, Professor Wieland, for the introduction, and thank you to the Institute for Monetary and Financial Stability for the opportunity to speak to you today.1 I come here at a moment of great challenge for Germany and Europe, and a moment in which it has never been more evident that the interests of Europe and the United States are closely aligned. America stands with Europe in defending Ukraine because we all understand that an assault on democracy in Europe is a threat to democracy everywhere. We also face the common challenge of excessive inflation, which is no coincidence, since Germany and other countries are dealing with many of the same forces driving up inflation in the United States.

Fortunately, in response to this moment of common challenges and interests, Europe and the United States have strengthened our ties and I believe we are more unified today than we have been for decades. We see that in the deepening and possible broadening of our security commitments, and we also see it in the strong commitment that central banks in Europe and elsewhere have made to fight inflation.

In today's distinguished lecture I will deal with two distinct topics, both of which I believe will be of interest. First, I will provide my outlook for the U.S. economy and how the Federal Reserve plans to reduce inflation and achieve our 2 percent target. Then I will pivot to a more academic discussion of the labor market and the possibility of a soft landing in which taming inflation does not harm employment.

Let me start with the economic outlook for the United States. Despite a pause early this year in the growth of real gross domestic product (GDP), the U.S. economy continues to power along at a healthy pace. The contraction in output reported in the first quarter was due to swings in two volatile categories, inventories and net exports, and I don't expect them to be repeated. Consumer spending and business investment, which are the bedrock of GDP, were both strong, and more recent data point toward solid demand and continuing momentum in the economy that will sustain output growth in the months ahead.

Another sign of strength is the labor market, which has created 2 million jobs in the first four months of 2022 at a remarkably steady pace that is down only slightly from the 562,000 a month last year. Unemployment is near a 50-year low, and both the low numbers of people filing for unemployment benefits and the high number of job openings indicate that the slowdown in the economy from the fast pace of last year isn't yet weighing on the job market. Some look at labor force participation, which is below its pre-COVID-19 level, as leaving a lot of room for improvement. However, there are underlying factors that explain why participation is depressed, including early retirements and individual choices associated with COVID concerns. Whatever the cause, low participation has contributed to the fact that there are two job vacancies for every one person counted looking for a job, a record high. Before the pandemic, when the labor market was in very solid shape, there was one vacancy for every two unemployed people. As I will explain, this very tight labor market has implications for inflation and the Fed's plans for reducing inflation. But on its own terms, we need to recognize that robust job creation is an underlying strength of the U.S. economy, which is expanding its productive capacity and supporting personal income and ongoing economic growth, in the face of other challenges.

Let me turn now to the outlook for the Fed's top priority, inflation. I said in December that inflation was alarmingly high, and it has remained so. The April consumer price index (CPI) was up 8.3 percent year over year. This headline number was a slight decline from 8.5 percent in March but primarily due to a drop in volatile gasoline prices that we know surged again this month. Twelve-month "core" inflation, which strips out volatile food and energy prices, was also down slightly to 6.2 percent in April, from 6.5 percent the month before, but the 0.6 percent monthly increase from March was an acceleration from the February to March rate and still too high. Meanwhile, the Fed's preferred measure based on personal consumption expenditures (PCE) recorded headline inflation of 6.3 percent and core of 4.9 percent. These lower readings relative to CPI reflect differences in the weights of various categories across these indexes. No matter which measure is considered, however, headline inflation has come in above 4 percent for about a year and core inflation is not coming down enough to meet the Fed's target anytime soon. Inflation this high affects everyone but is especially painful for lower- and middle-income households that spend a large share of their income on shelter, groceries, gasoline, and other necessities. It is the FOMC's job to meet our price stability mandate and get inflation down, and we are determined to do so.

The forces driving inflation today are the same ones that emerged a year ago. The combination of strong consumer demand and supply constraints—both bottlenecks and a shortage of workers relative to labor demand—is generating very high inflation. We can argue about whether supply or demand is a greater factor, but the details have no bearing on the fact that we are not meeting the FOMC's price stability mandate. What I care about is getting inflation down so that we avoid a lasting escalation in the public's expectations of future inflation. Once inflation expectations become unanchored in this way, it is very difficult and economically painful to lower them.

While it is not surprising that inflation expectations for the next year are up, since current inflation is high, what I focus on is longer-term inflation expectations. Recent data that try to measure longer-term expectations are mixed. Overall, my assessment is that longer-range inflation expectations have moved up from a level that was consistent with trend inflation below 2 percent to a level that's consistent with underlying inflation a little above 2 percent. I will be watching that these expectations do not continue to rise because longer-term inflation expectations influence near term inflation, as well as our ability to achieve our 2 percent target. When they are anchored, they influence spending decisions today in a way that helps inflation move toward our target. To ensure these longer-term expectations do not move up broadly, the Federal Reserve has tools to reduce demand, which should ease inflation pressures. And, over time, supply constraints will resolve to help rein in price increases as well, although we don't know how soon.

I cannot emphasize enough that my FOMC colleagues and I are united in our commitment to do what it takes to bring inflation down and achieve the Fed's 2 percent target. Since the start of this year, the FOMC has raised the target range for the federal funds rate by 75 basis points, with 50 basis points of that increase coming at our meeting earlier this month. We also issued forward guidance about the likely path of policy. The May FOMC statement said the Committee "anticipates that ongoing increases in the target range will be appropriate."

I support tightening policy by another 50 basis points for several meetings. In particular, I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation. This is my projection today, given where we stand and how I expect the economy to evolve. Of course, my future decisions will depend on incoming data. In the next couple of weeks, for example, the May employment and CPI reports will be released. Those are two key pieces of data I will be watching to get information about the continuing strength of the labor market and about the momentum in price increases. Over a longer period, we will learn more about how monetary policy is affecting demand and how supply constraints are evolving. If the data suggest that inflation is stubbornly high, I am prepared to do more.

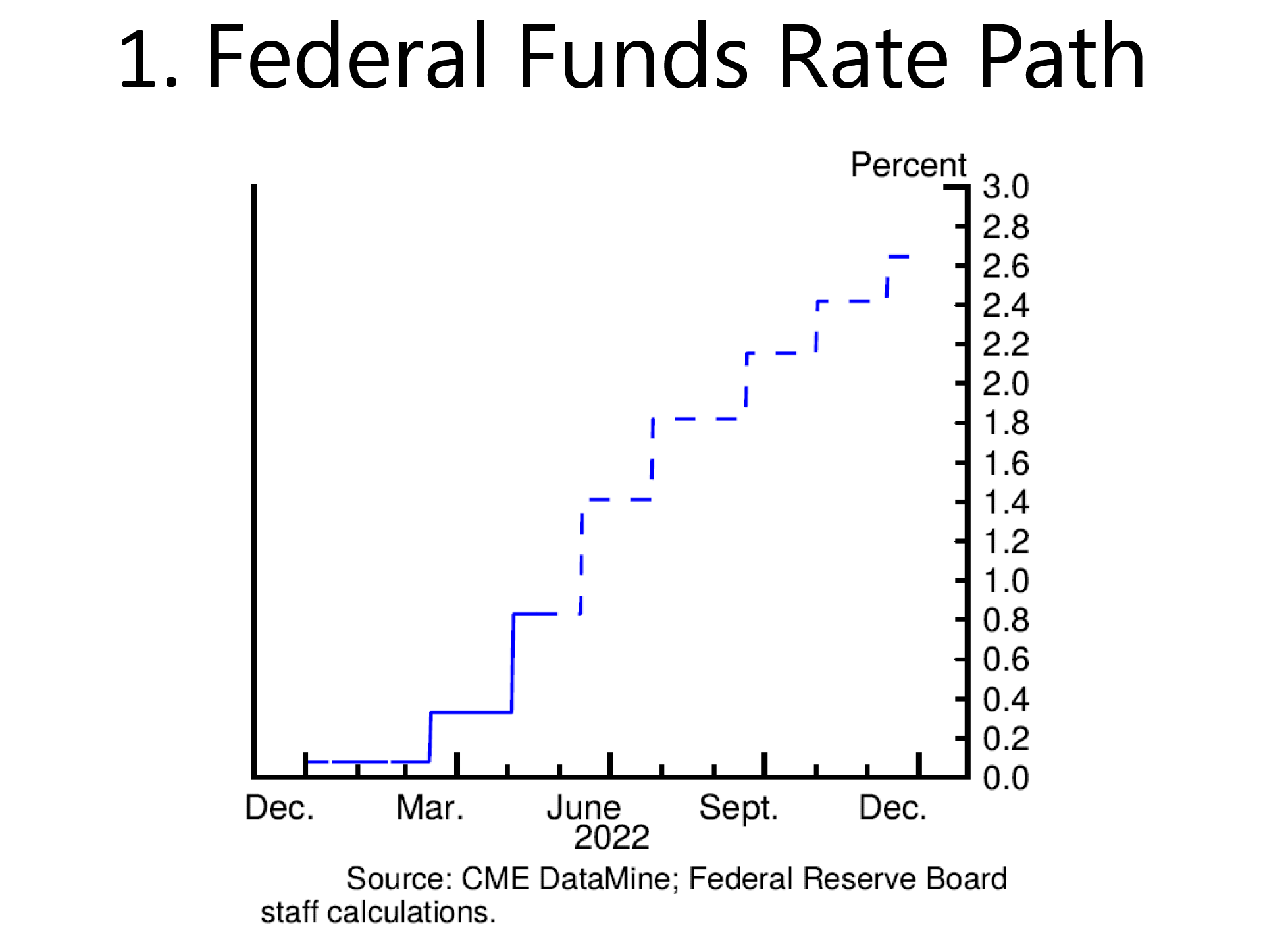

My plan for rate hikes is roughly in line with the expectations of financial markets. As seen in slide 1, federal funds futures are pricing in roughly 50 basis point hikes at the FOMC's next two meetings and expecting the year-end policy rate to be around 2.65 percent. So, in total, markets expect about 2.5 percentage points of tightening this year. This expectation represents a significant degree of policy tightening, consistent with the FOMC's commitment to get inflation back under control and, if we need to do more, we will.

{kind=link}

These current and anticipated policy actions have already resulted in a significant tightening of financial conditions. The benchmark 10-year Treasury security began the year at a yield of around 1.5 percent and has risen to around 2.8 percent. Rates for home mortgages are up 200 basis points, and other credit financing costs have followed suit. Higher rates make it more expensive to finance spending and investment which should help reduce demand and contribute to lower inflation.

In addition to raising rates, the FOMC further tightened monetary policy by ending asset purchases in March and then agreeing to start reducing our holdings of securities, a process that begins June 1. By allowing securities to mature without reinvesting them, the Fed's balance sheet will shrink. We will phase in the amount of redemptions over three months. By September, we anticipate having up to $95 billion of securities rolling off the Fed's portfolio each month. This pace will reduce the Fed's securities holdings by about $1 trillion over the next year, and the reductions will continue until securities holdings are deemed close to the ample levels needed to implement policy efficiently and effectively. Although estimates are highly uncertain, using a variety of models and assumptions, the overall reduction in the balance sheet is estimated to be equivalent to a couple of 25-basis-point rate hikes.

All these actions have the goal of bringing inflation down toward the FOMC's 2 percent target. Increased rates and a smaller balance sheet raise the cost of borrowing and thus reduce household and business demand. On top of this, I also hope that over time supply problems resolve and help lower inflation. But the Fed isn't waiting for these supply constraints to resolve. We have the tools and the will to make substantial progress toward our target.

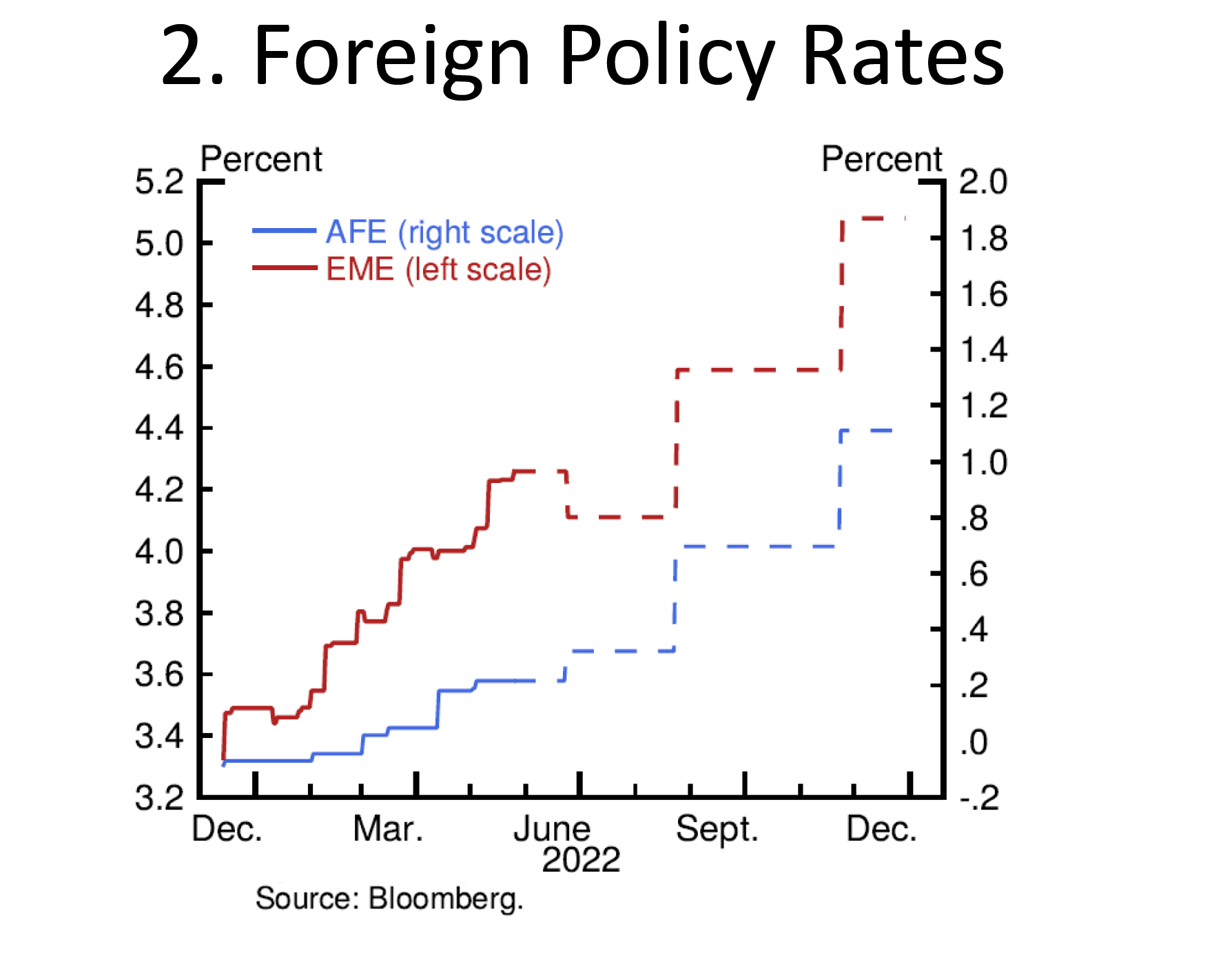

The United States is not alone in facing excessive inflation, and other central banks also are responding. There is a global shift toward monetary tightening. In the euro area, headline inflation continued to edge up in April, to 7.5 percent, while its version of core inflation increased from 2.9 percent to 3.5 percent. Based on this broadening of price pressures, communication by the European Central Bank (ECB) is widely interpreted as signaling that it will likely start raising its policy rate this summer and that it could raise rates a few times before year-end. Policy tightening started last year, as emerging markets including Mexico and Brazil increased rates substantially amid expectations of accelerating inflation. Several advanced-economy central banks, including the Bank of England, began raising interest rates in the second half of last year. Like the Fed, the Bank of Canada lifted off in March and, also like the Fed, picked up the pace of tightening with a rate hike of 50 basis points at its most recent meeting. Central banks in Australia and Sweden pivoted sharply to hike rates at their most recent meetings after previously saying that such moves were not likely anytime soon.

Slide 2 shows the similarly timed policy responses across advanced and emerging economy central banks in terms of actual and anticipated increases in their policy rates. Emerging market economies started the year with a policy rate that averaged around 3.5 percent, and they are expected to end the year averaging a bit over 5 percent. Advanced foreign economies started a bit below zero and at this point are expected to move up, on average, by around 1 percentage point. This worldwide increase in policy rates, unfortunately, reflects the fact that high inflation is a global problem, which central banks around the world recognize must be addressed.

{kind=link}

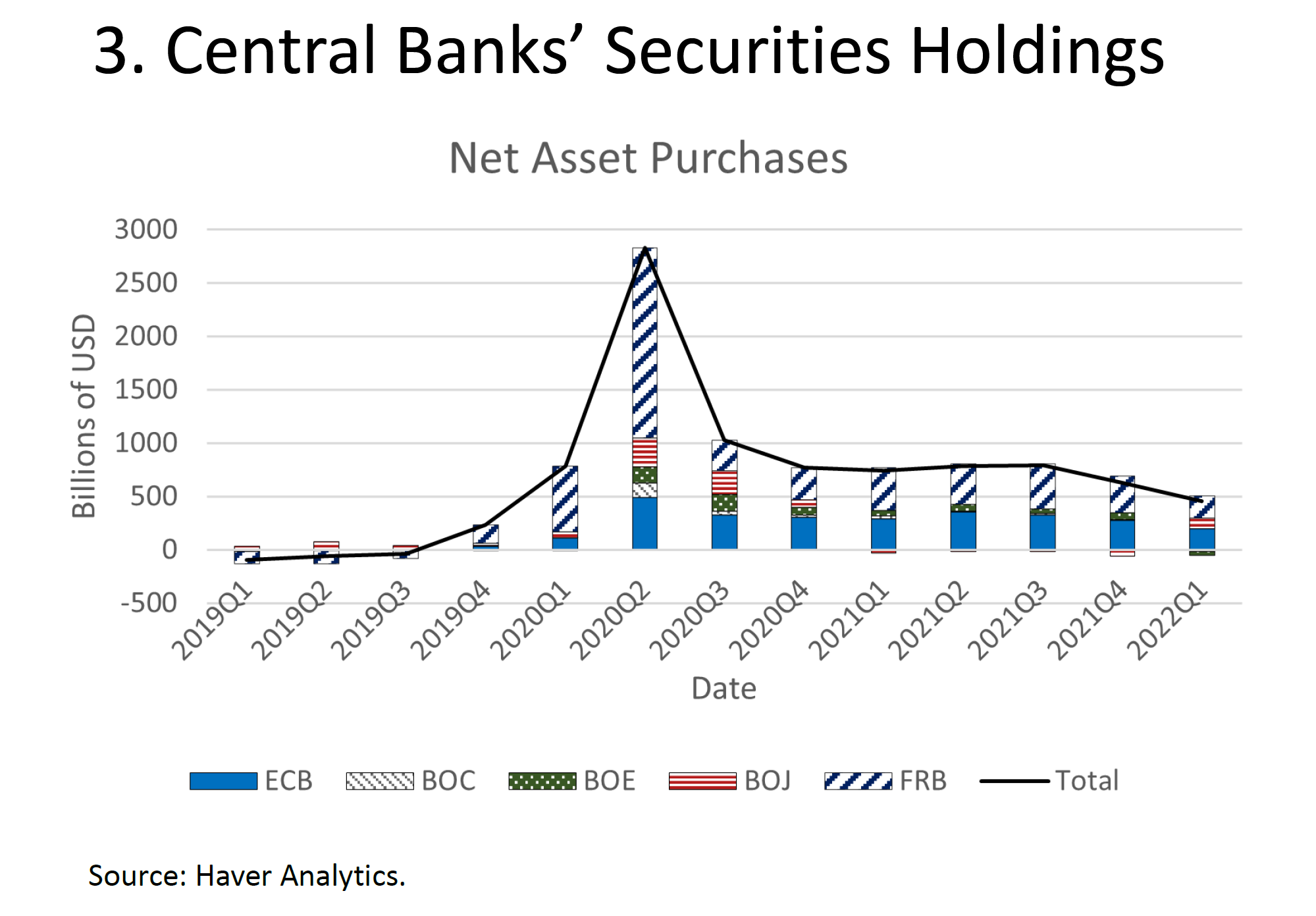

Finally, like the Fed, many other advanced-economy central banks that expanded their balance sheets over the past two years are now reversing course. In recent months, as shown in slide 3, the Bank of Canada and Bank of England have begun to shrink their balance sheets by stopping full reinvestment of maturing assets, similar to what the Fed will commence in June. Although the ECB has committed to reinvesting maturing assets for quite some time, it has tapered net purchases substantially since last year and has indicated it will likely end those purchases early in the third quarter.

{kind=link}

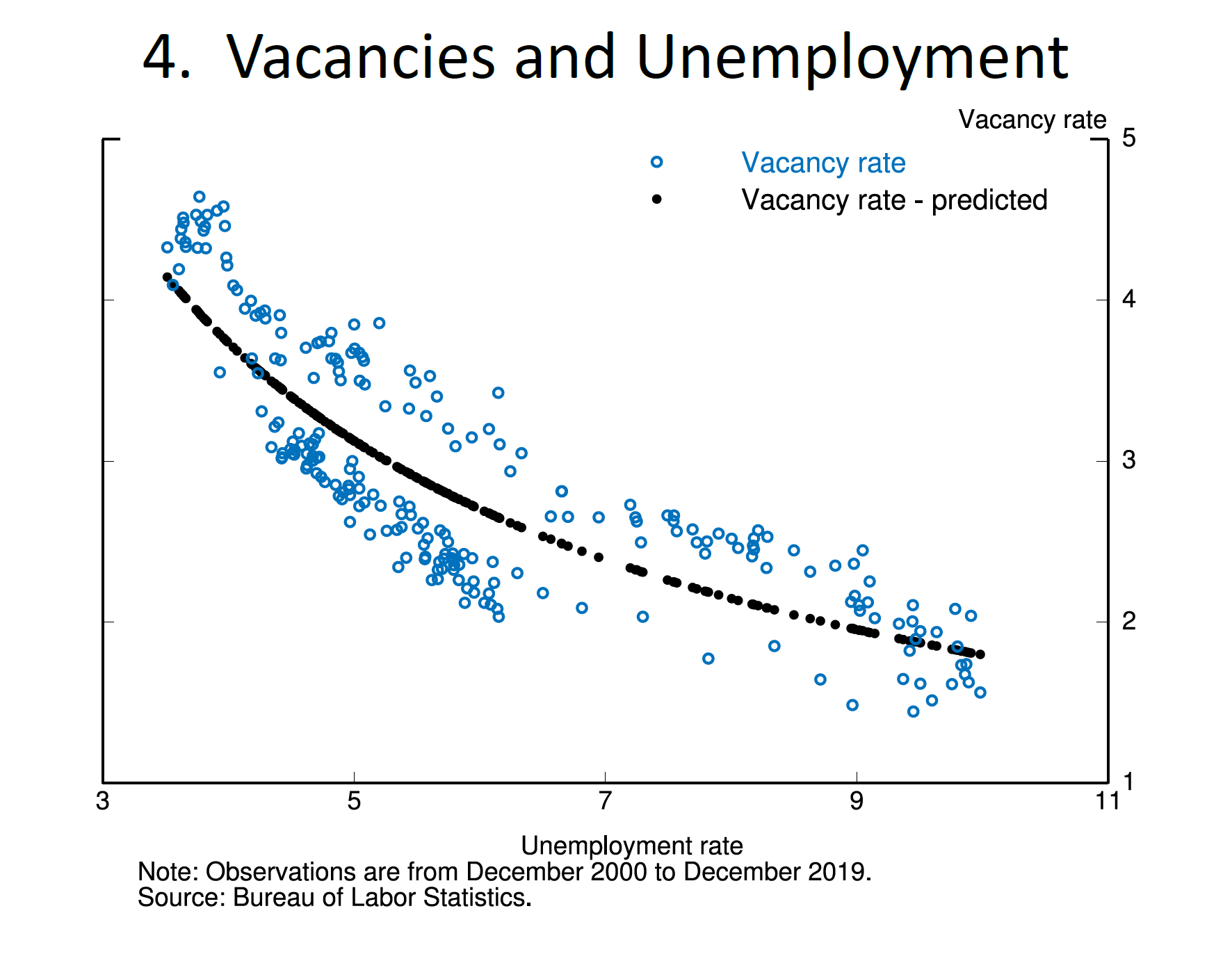

Some have expressed concern that the Fed cannot raise interest rates to arrest inflation while also avoiding a sharp slowdown in economic growth and significant damage to the labor market. One argument in this regard warns that policy tightening will reduce the current high level of job vacancies and push up unemployment substantially, based on the historical relationship between these two pieces of data, which is depicted by something called the Beveridge curve. Because I am now among fellow students of economics, I wanted to take a moment to show why this statement may not be correct in current circumstances.

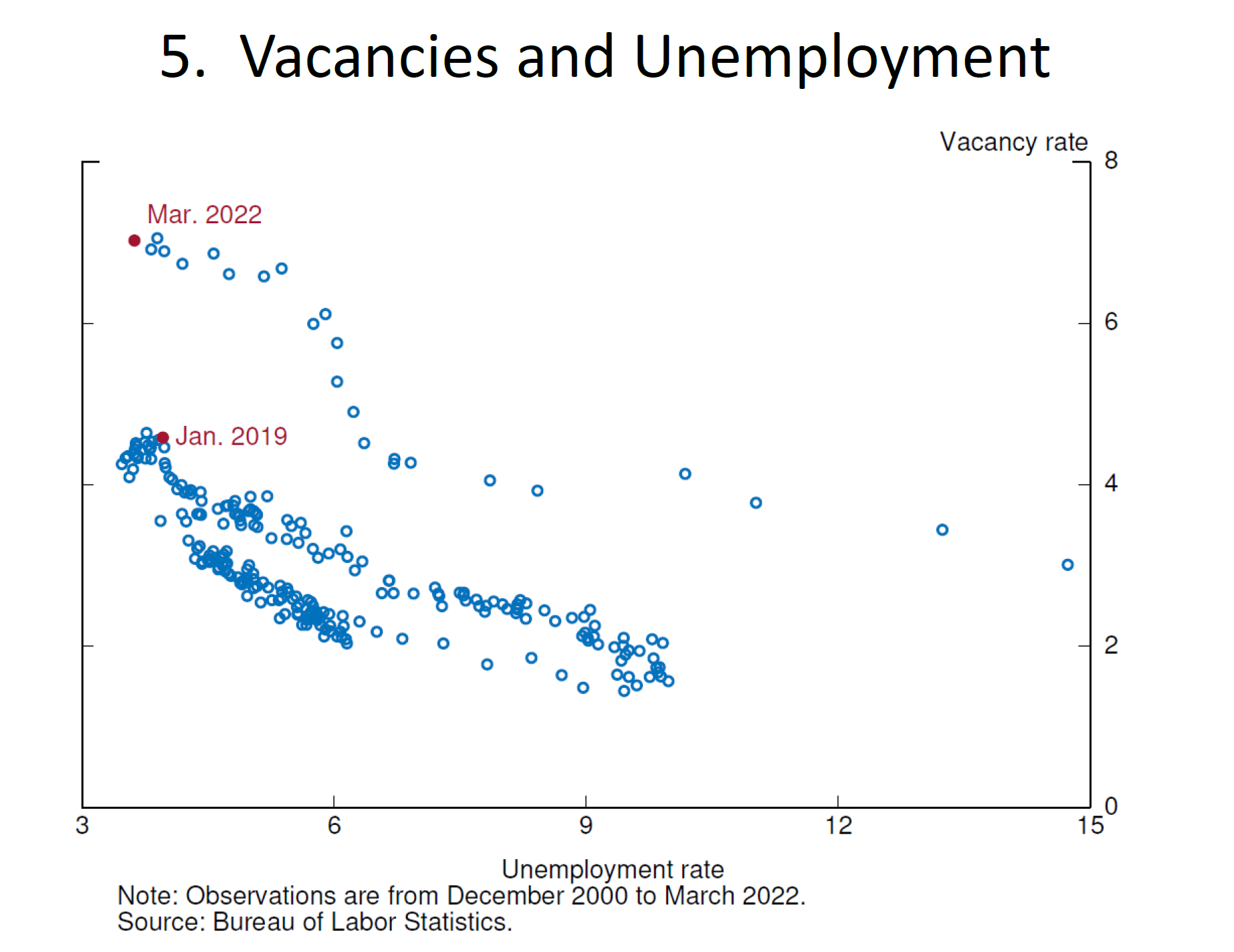

First, a little background. The relationship between vacancies and the unemployment rate is shown in slide 4. The blue dots in the figure show observations of the vacancy rate and the unemployment rate between 2000 and 2018. The black curve is the fitted relationship between the log of vacancies and the log of unemployment over this period. It has a somewhat flat, downward slope. From this, the argument goes, policy to slow demand and push down vacancies requires moving along this curve and increasing the unemployment rate substantially.

{kind=link}

But there's another perspective about what a reduction in vacancies implies for unemployment that is just as plausible, if not more so. Slide 5 shows the same observations as slide 4 but also adds observations from the pandemic. The two larger red dots show the most recent observation, March 2022, and January 2019, when the vacancy rate had achieved its highest rate before the pandemic. These two dots suggest that the vacancy rate can be reduced substantially, from the current level to the January 2019 level, while still leaving the level of vacancies consistent with a strong labor market and with a low level of unemployment, such as we had in 2019. To see why this is a plausible outcome, I first need to digress a bit to discuss the important determinants of unemployment.

{kind=link}

Many factors influence the unemployment rate, and vacancies are just one. Thus, to understand how a lower vacancy rate would influence unemployment going forward, we need to separate the direct effect of vacancies on the unemployment rate from other factors. To do that, we first need to review the factors that account for unemployment movements.

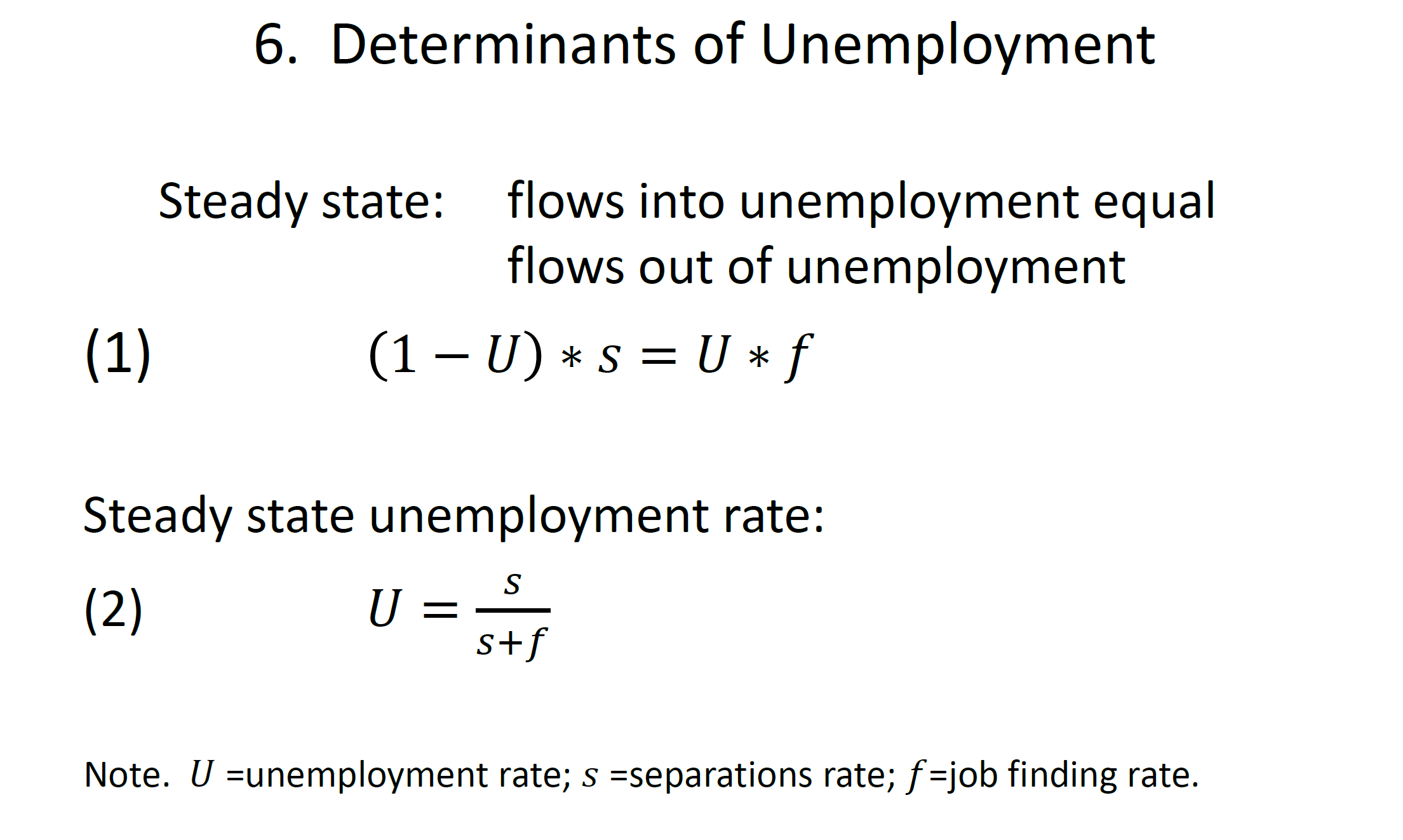

There are two broad determinants of unemployment: separations from employment (including layoffs and quits), which raise unemployment, and job finding by the unemployed, which lowers unemployment.2 Separations consist largely of layoffs, which are typically cyclical, surging in recessions and falling during booms. Job finding is also highly cyclical, rising as the labor market tightens and falling in recessions.

To see how separations and job finding affect the unemployment rate, it's helpful to start with equation (1) on slide 6, which states that in a steady state (that is, when the unemployment rate is constant), flows into unemployment, the left side of equation (1), must equal flows out of unemployment, the right side. Flows into unemployment equal the separations rate, $$s$$, times the level of employment. For simplicity, I've normalized the labor force to 1, so that employment equals 1 minus unemployment, $$U$$. Flows out of unemployment, the right side of the equation, equal the rate of job finding, $$f$$, times the number of unemployed. Rearranging this equation yields an expression for the steady-state unemployment rate, equation (2).3 Because flows into and out of unemployment are quite high, the actual unemployment rate converges to the steady-state unemployment rate quickly, and the steady-state unemployment rate typically tracks the actual rate closely.4 So, going forward, I'm going to think of the steady-state unemployment rate as a good approximation of the actual unemployment rate.

{kind=link}

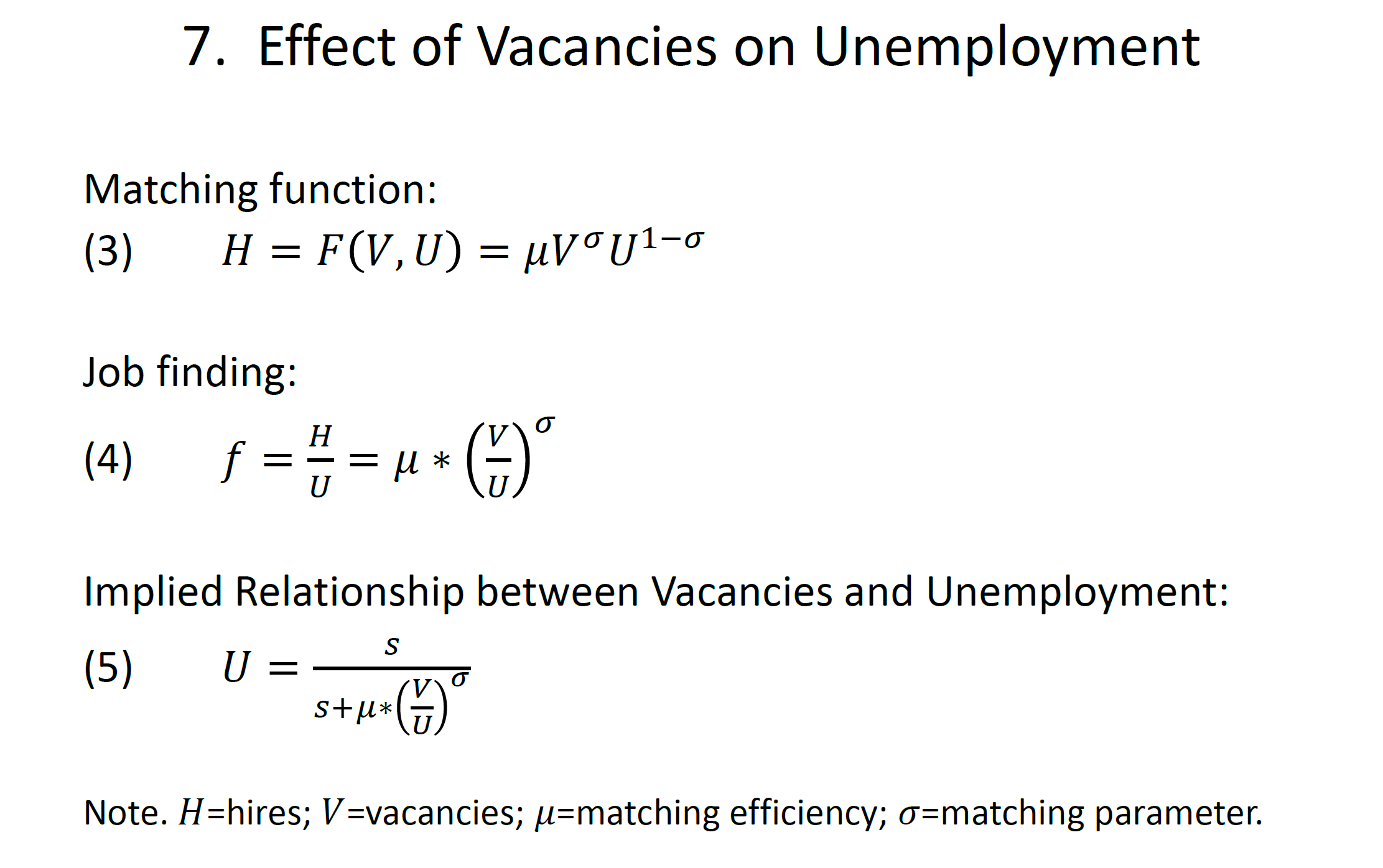

Now let me focus on job finding, which is often thought to depend on the number of job vacancies relative to the number of unemployed workers. To see why, start with equation (3) on slide 7, which states that the number of hires is an increasing function of both the number of job vacancies and the number of unemployed individuals searching for jobs: The more firms there are looking for workers and the more workers there are looking for jobs, the more matches, or hires, there will be. For convenience, I'm assuming a mathematical representation of this matching function takes a Cobb-Douglas form. If we divide both sides of equation (3) by unemployment, we get equation (4), which expresses the job-finding rate as a function of the ratio of vacancies to unemployment, or labor market tightness.

{kind=link}

Because we have data for both the left and right sides of equation (4), we can estimate it and obtain parameter values for the elasticity of job finding with respect to labor market tightness, sigma, and matching efficiency, mu.5 Matching efficiency represents factors that can increase (or decrease) job findings without changes in labor market tightness. On the one hand, if the workers searching for jobs are well suited for the jobs that are available, matching efficiency will be high; on the other hand, if many searching workers are not well suited for the available jobs, matching efficiency will be low.6

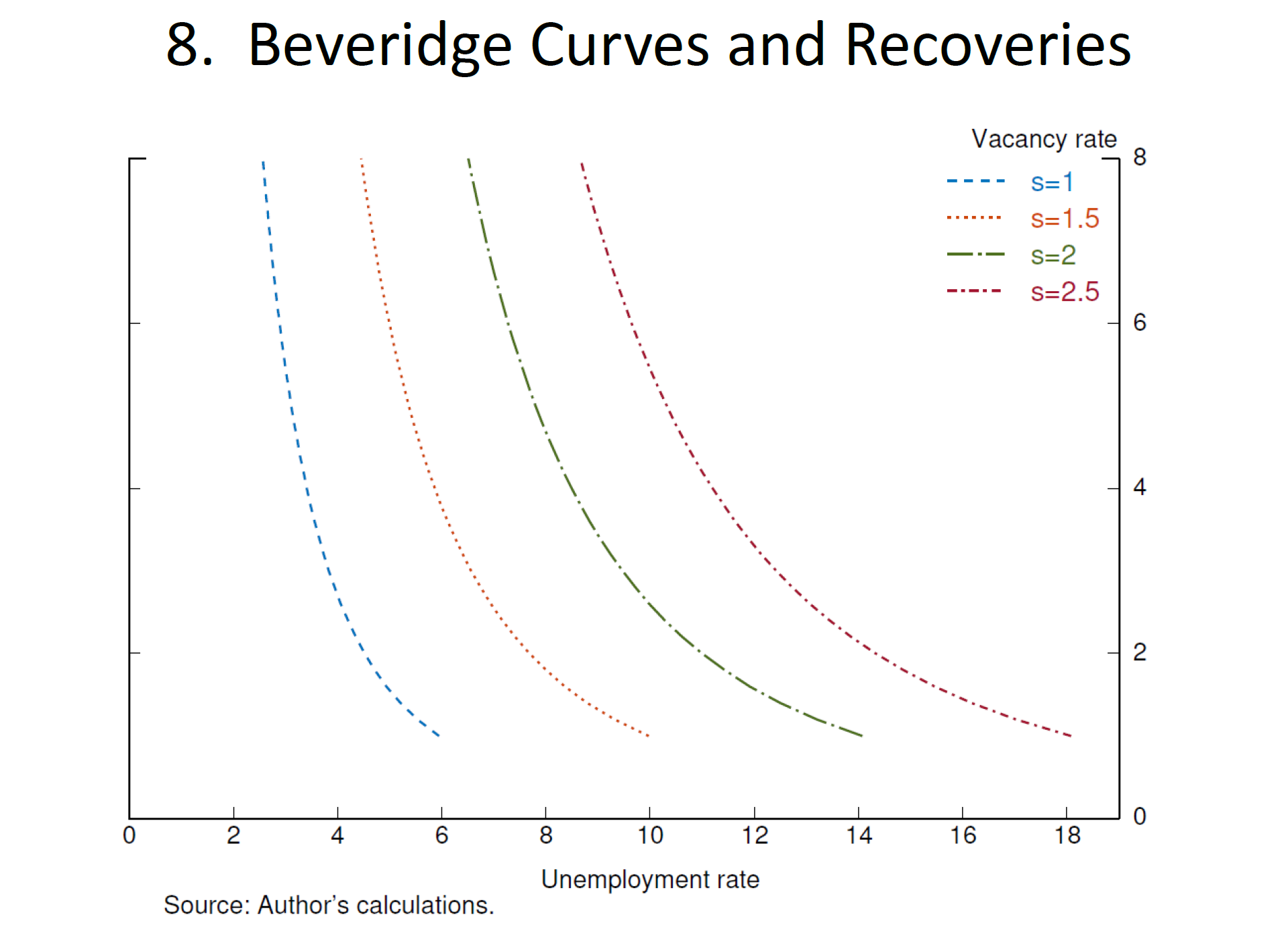

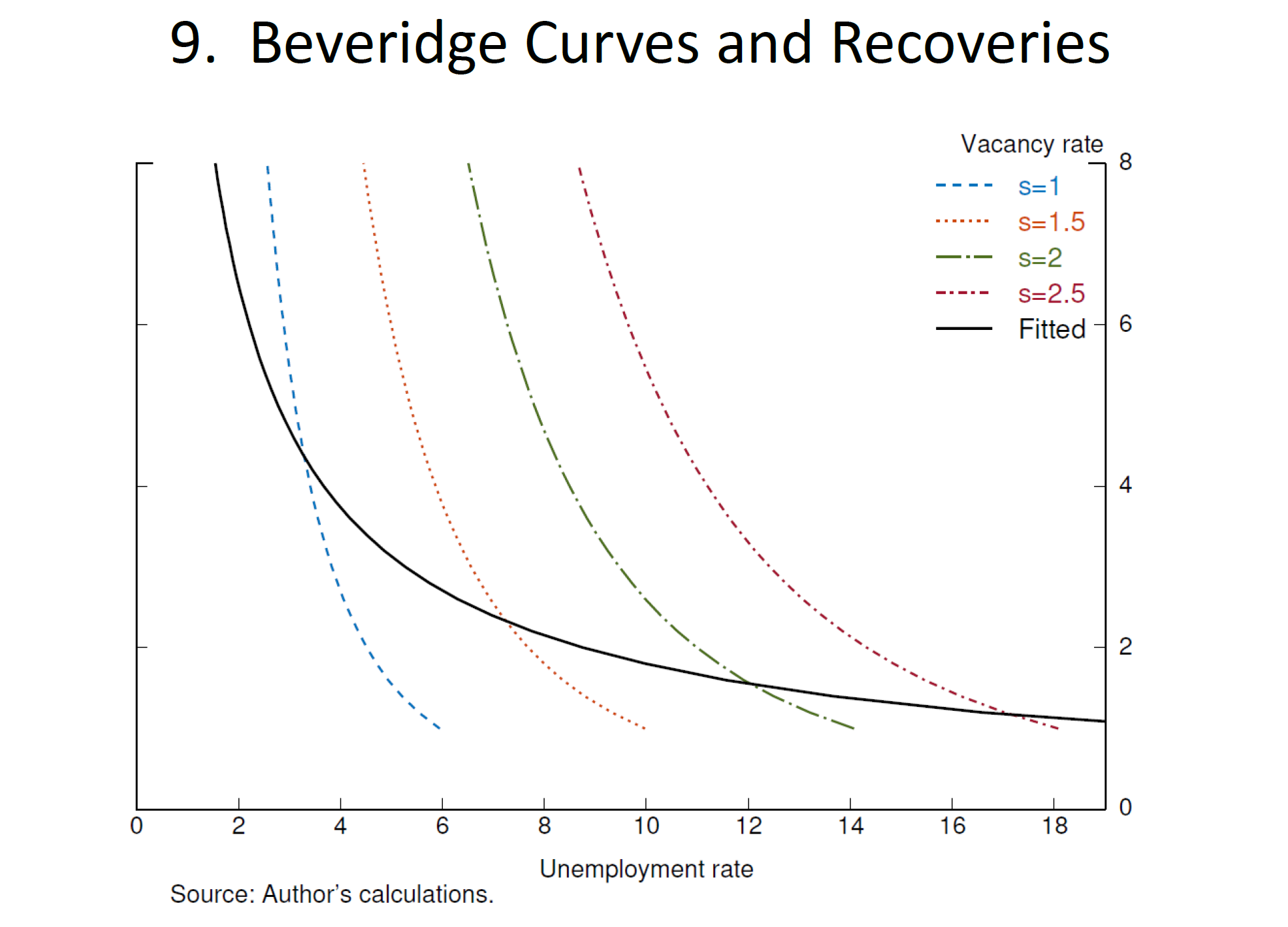

The last step is to plug our expression for job finding into equation (2), the steady-state unemployment rate, yielding equation (5). Equation (5) shows how vacancies affect the unemployment rate. To illustrate this relationship, I solve equation (5) for different values of $$V$$ and $$s$$, holding the matching efficiency parameters constant. That is, I pick a separation rate at some level and trace out what happens to the unemployment rate as the vacancy rate changes. Then I pick a different separation rate and again trace out the effect of vacancies on unemployment. The result is shown on slide 8, which plots four curves showing the effect of vacancies on unemployment for four different separation rates. Each curve is convex; as the number of vacancies increases relative to the number of individuals looking for work, it becomes harder for firms to fill jobs with suitable workers, and more jobs remain vacant. This is exactly the situation many employers are now experiencing. Because more vacancies generate fewer and fewer hires, they result in smaller and smaller reductions in unemployment. But large numbers of vacancies are, of course, a hallmark of tight labor markets and additional vacancies continue to strongly boost wage growth and quits.

{kind=link}

The curve farthest to the right, labeled s=2.5, represents a situation when the separations rate is 2.5 percent, a historically high level. This rate is approximately the level seen in the middle of 2020, just after the onset of the pandemic. You can see that when the separations rate is this high, the unemployment rate is also going to be high, no matter the level of vacancies.

Now let's think about what happens as the economy recovers, as it has over the past two years. In an expansion, layoffs fall, pushing down separations and moving the curve to the left. At the same time, greater labor demand increases vacancies, causing the labor market to move up the steep curves. The combination of these movements is shown in slide 9 as the black fitted curve, which I've reproduced from slide 4. As you recall, the black curve fits the actual observations on unemployment and vacancies we saw before the pandemic. And we now can see that these observations are produced by a combination of changes in vacancies and separations (as well as other influences on unemployment). Decreases in the separations rate reduce the unemployment rate without changing vacancies, imparting a flatness to the fitted curve relative to the steeper curves that only reflect the effect of vacancies. If we want to just focus on the effect of vacancies, then we should be looking at the steep curves, especially when the labor market is tight, as it is now.

{kind=link}

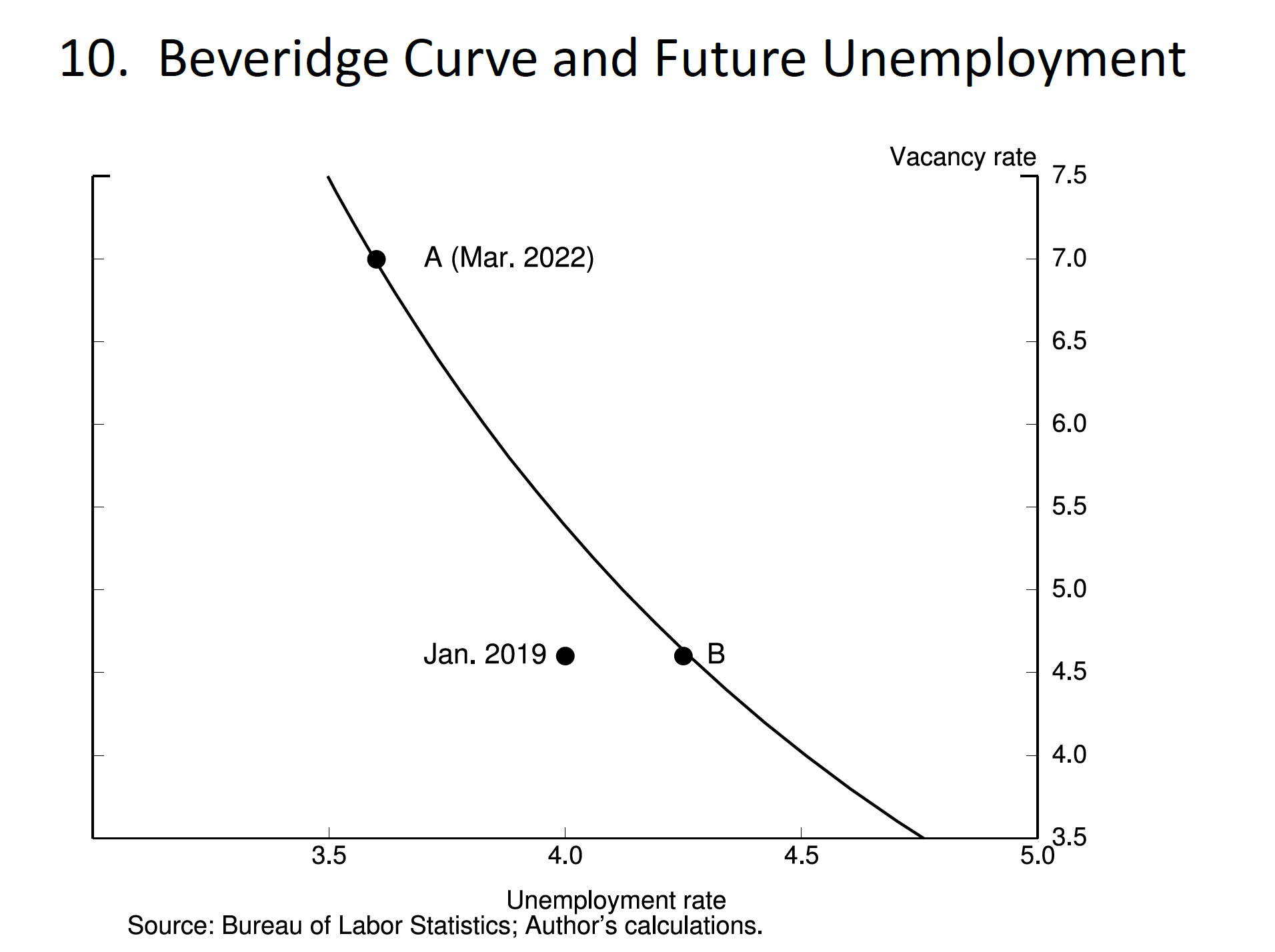

What does all this suggest about what will happen to the labor market when, as I expect, a tightening of financial conditions and fading fiscal stimulus start to cool labor demand? Slide 10 focuses on the Beveridge curve (the relationship produced by the direct effect of changes in vacancies on unemployment) when the separations rate is low, as it is now.7 The March 2022 observation lies at the top of the curve and is labeled point A. If there is cooling in aggregate demand spurred by monetary policy tightening that tempers labor demand, then vacancies should fall substantially. Suppose they decrease from the current level of 7 percent to 4.6 percent, the rate prevailing in January 2019, when the labor market was still quite strong. Then we should travel down the curve from point A to point B.8 The unemployment rate will increase, but only somewhat because labor demand is still strong—just not as strong—and because when the labor market is very tight, as it is now, vacancies generate relatively few hires. Indeed, hires per vacancy are currently at historically low levels. Thus, reducing vacancies from an extremely high level to a lower (but still strong) level has a relatively limited effect on hiring and on unemployment.

{kind=link}

Now, I also show the January 2019 observation of vacancies and unemployment. Recall, this is also where the economy was over the year prior to the pandemic. As you can see, moving from the March 2022 observation to the January 2019 observation is not that different from the change in the unemployment rate predicted by my estimated Beveridge curve, which suggests the predicted small increase in unemployment is a plausible outcome to policy tightening.

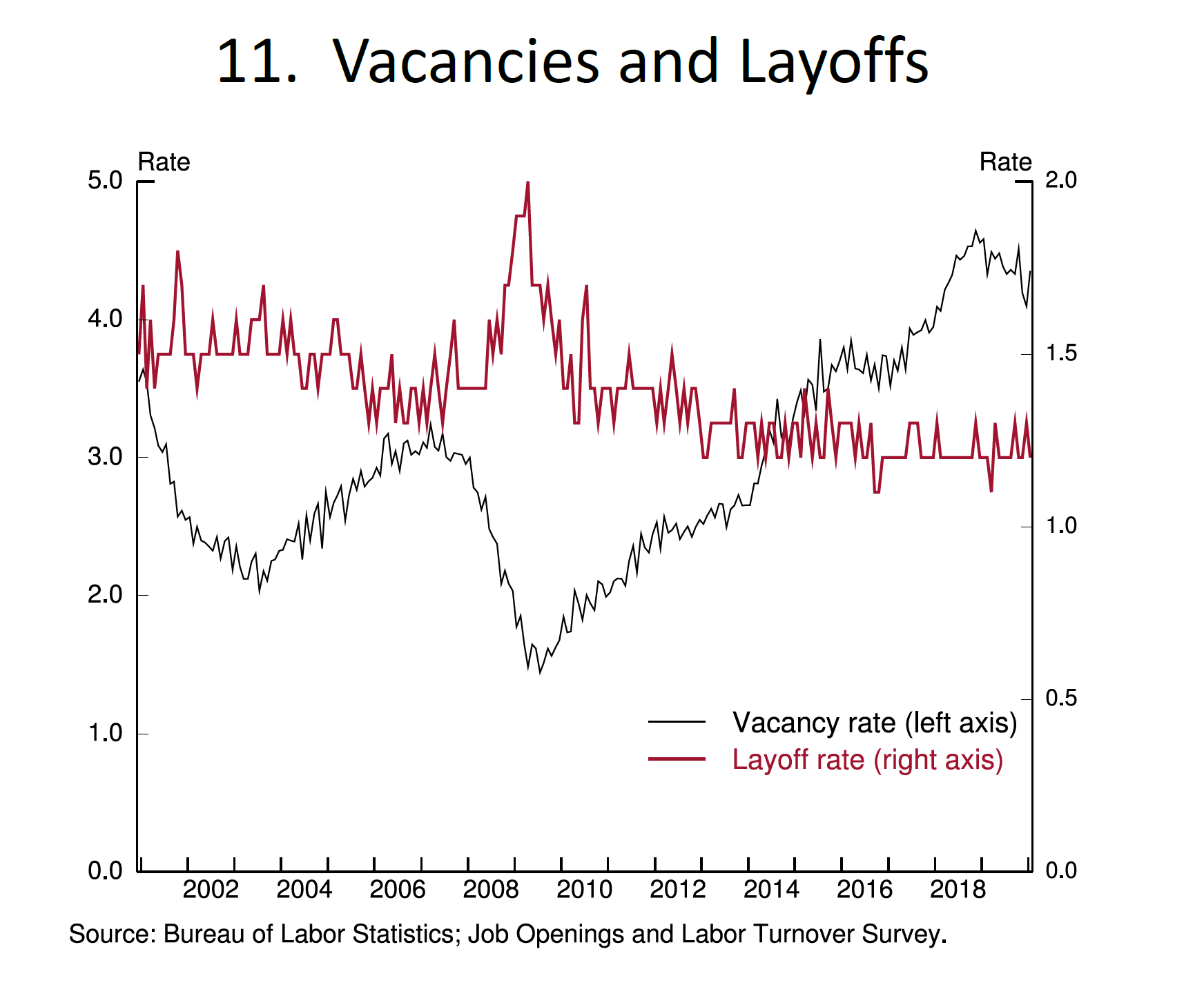

If labor demand cools, will separations increase and shift the curve outward, increasing unemployment further? I don't think so. As shown on slide 11, outside of recessions, layoffs don't change much. Instead, changes in labor demand appear to be reflected primarily in changes in vacancies.

{kind=link}

Now, it's certainly possible, even probable, that influences on the unemployment rate other than vacancies will change going forward. In terms of the equations we have been discussing, layoffs could increase somewhat, instead of staying constant. Matching efficiency could also improve or deteriorate. The vacancy rate could also change more or less than I have assumed. Thus, I'm not arguing that the unemployment rate will end up exactly as the Beveridge curve I've drawn suggests. But I do think it quite plausible that the unemployment rate will end up in the vicinity of what the Beveridge curve currently predicts.

Another consideration is that non-linear dynamics could take hold if the unemployment rate increases by a certain amount, as suggested by the Sahm rule, which holds that recessions have in the past occurred whenever the three-month moving average of the unemployment rate rises 0.5 percentage point over its minimum rate over the previous 12 months.9 We certainly need to be alert to this possibility, but the past is not always prescriptive of the future. The current situation is unique. We've never seen a vacancy rate of 7 percent before. Reducing the vacancy rate by 2.5 percentage points would still leave it at a level seen at the end of the last expansion, whereas in previous expansions a reduction of 2.5 percent would have left vacancies at or below 2 percent, a level only seen in extremely weak labor markets.

To sum up, the relationship between vacancies and unemployment gives me reason to hope that policy tightening in current circumstances can tame inflation without causing a sharp increase in unemployment. Of course, the path of the economy depends on many factors, including how the Ukraine war and COVID-19 evolve. From this discussion, I am left optimistic that the strong labor market can handle higher rates without a significant increase in unemployment.

In closing, I want to again thank the institute for the invitation to address you today, at a time of considerable challenge for Germany and the United States. It's not the first time we have faced such moments together. Just south of the Frankfurt Airport is a surprising sight—a couple of antique military cargo planes, parked on the side of the Autobahn. They were built by Douglas Aircraft, nearly 80 years ago, and stand today as monuments to one of the greatest achievements of cooperation between the freedom-loving people of Europe and those of the United States.

For 11 months, these two planes, and many others, took off and landed in perpetual motion, delivering 2.3 million tons of food, fuel, and other essentials to the people of Berlin, who were surrounded and besieged by Soviet forces. The commitment and ultimate triumph of this improbable airlift was in many ways the beginning of an alliance that has included ongoing economic cooperation that has strengthened both our democracies. In that spirit, I am certain we can both overcome the economic challenges that lie ahead.

References

Ahn, Hie Joo, and Leland Crane (2020). "Dynamic Beveridge Curve Accounting," Finance and Economics Discussion Series 2020-027. Washington: Board of Governors of the Federal Reserve System, March.

Ahn, Hie Joo, and James Hamilton (2020). "Heterogeneity and Unemployment Dynamics," Journal of Business & Economic Statistics, vol. 38 (July), pp. 554–69.

Barnichon, Regis, and Andrew Figura (2015). "Labor Market Heterogeneity and the Aggregate Matching Function," American Economic Journal: Macroeconomics, vol. 7 (October), pp. 222–49.

Elsby, Michael, Bart Hobijn, and Aysegul Sahin (2015). "On the Importance of the Participation Margin for Labor Market Fluctuations," Journal of Monetary Economics, vol. 72 (May), pp. 64–82.

Elsby, Michael, Ryan Michaels, and David Ratner (2015). "The Beveridge Curve: A Survey," Journal of Economic Literature, vol. 53 (September), pp. 571–630.

Elsby, Michael, Ryan Michaels, and Gary Solon (2009). "The Ins and Outs of Cyclical Unemployment," American Economic Journal: Macroeconomics, vol. 1 (January), pp. 84–110.

Fujita, Shigeru, and Garey Ramey (2009). "The Cyclicality of Separation and Job Finding Rates," International Economic Review, vol. 50 (May), pp. 415–30.

Sahm, Claudia (2019). "Direct Stimulus Payments to Individuals (PDF)," report. Washington: Brookings Institution, May.

Shimer, Robert (2012). "Reassessing the Ins and Outs of Unemployment," Review of Economic Dynamics, vol. 15 (April), pp. 127–48.

1. I am grateful to Andrew Figura for assistance in preparing the Beveridge curve material. These remarks represent my own views and not any position of the Federal Reserve Board or the Federal Open Market Committee. Return to text

2. For simplicity, I am ignoring flows into and out of the labor force, which can also influence the unemployment rate; see Elsby, Hobijn and Sahin (2015). Return to text

3. If the labor force is allowed to vary, then the expression is similar but somewhat more complicated. Return to text

4. For more on decomposing unemployment rate movements, see Shimer (2012); Elsby, Michaels and Solon (2009); Fujita and Ramey (2009); and Ahn and Crane (2020). Return to text

5. I will assume levels of $$\mu$$ and $${\sigma}$$ that are consistent with regressions of log($$\frac{H}{U}$$) on log($$\frac{V}{U}$$) using data on unemployment, JOLTS job openings, and transitions from unemployment into employment from 2009 to 2019. Specifically, I assume that $$\mu=0.27$$, and $${\sigma}=0.3$$. Return to text

6. For more on the effect of matching efficiency on unemployment and the Beveridge curve, see Barnichon and Figura (2015); Elsby, Michaels, and Ratner (2015); and Ahn and Hamilton (2020). Return to text

7. Specifically, I set the separations rate equal to 1.23 percent, a little above current levels. Return to text

8. The unemployment rate found on the slide is not a prediction and simply an illustrative example. Return to text

9. For more information on the Sahm rule, see Sahm (2019). Return to text

"soft" - Google News

May 30, 2022 at 10:05PM

https://ift.tt/hOuvCt4

Speech by Governor Waller on the economic outlook and thoughts on a soft landing - Federal Reserve

"soft" - Google News

https://ift.tt/UjIaP8B

https://ift.tt/arS9GlF

Bagikan Berita Ini

0 Response to "Speech by Governor Waller on the economic outlook and thoughts on a soft landing - Federal Reserve"

Post a Comment