The latest wave of U.S. economic data suggest that growth remains strong even as excessive inflation persists. The interest rates that made sense in the 2010s may no longer apply.

One might have thought that the combination of post-pandemic fiscal tightening and Federal Reserve interest rate increases would have done something to slow down the U.S. economy. We cannot know the counterfactual, but at least on the surface, one would have been wrong.

Production of goods and services rose at a 3% yearly rate in 2022H2. The data we have so far for January suggests that the economy is sustaining that pace, and may be accelerating from there, with booming growth in employment, hours, manufacturing production, and retail spending. The housing market remains depressed—compared to the 2021 boom, at any rate—in the face of higher interest rates and the end of the pandemic-related migration spike, but even that has failed to translate into slowing employment in construction and real estate. Meanwhile, nominal income growth and inflation continue to come in hotter than is consistent with the Fed’s stated preference for 2% yearly price increases.

The good news is that the humming economy continues to provide more opportunities for more people to produce more of the things we need and want. The bad news is that it seems increasingly unlikely that America will return to pre-pandemic inflation rates without a downturn.1

One implication, regardless of whether officials choose to accommodate the new reality or fight it, is that interest rates may need to rise more than many people (including me) had been expecting back in the summer. That presents an interesting disconnect vis. the recent decline in real yields, which may be due to technical factors associated with the Fed’s balance sheet.

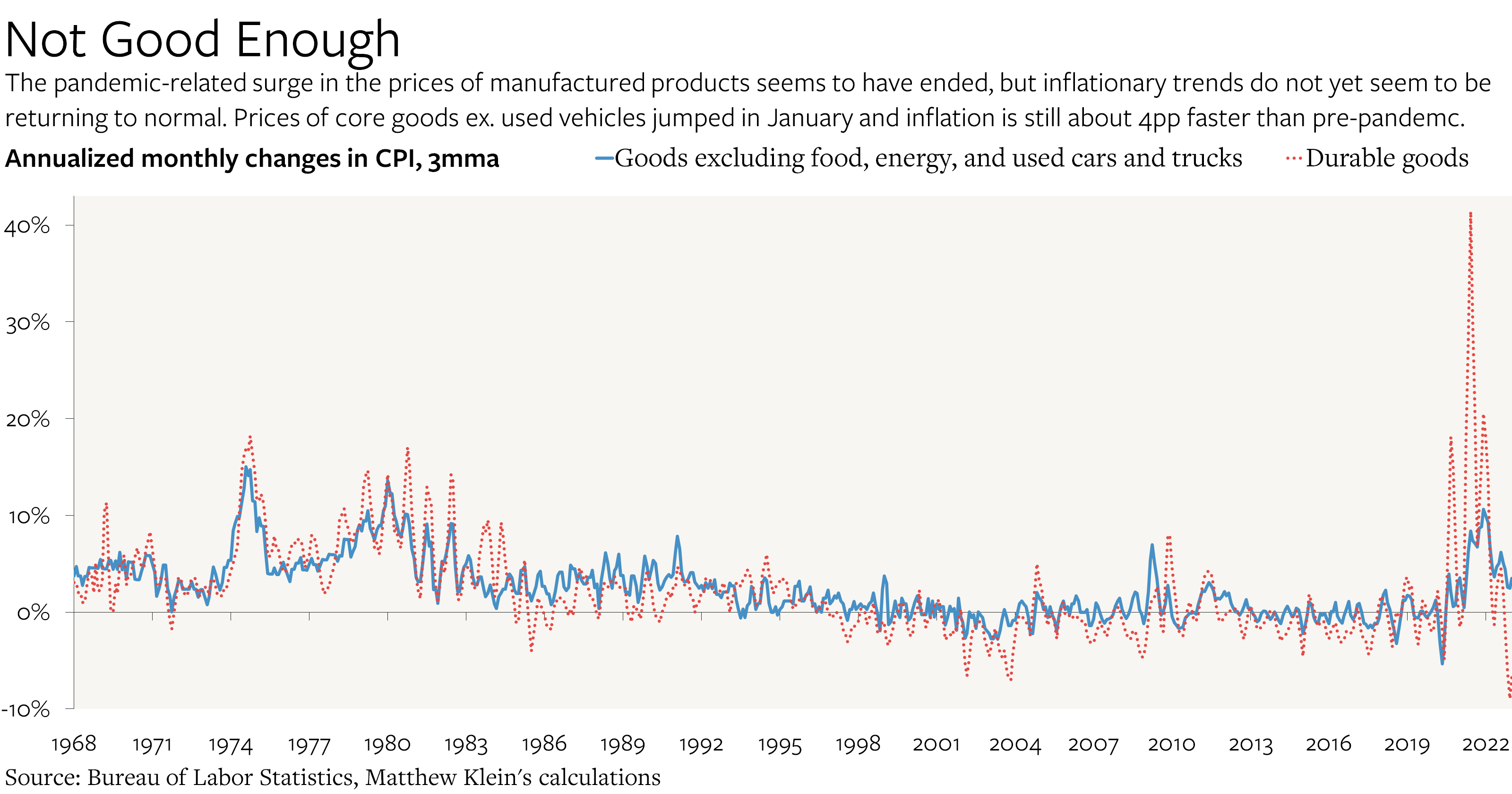

The End of Goods Deflation?

January’s Consumer Price Index (CPI) contained several bits of unwelcome news. Perhaps most surprising was the unwelcome return of inflation for manufactured goods. Prices of commodities excluding food, energy, and used vehicles rose by 0.5% on a seasonally-adjusted basis relative to December. That was the biggest one-month gain since August. Prices of these items had been essentially flat in the decade before the pandemic, but rose more than 7% annualized from March 2021-June 2022. Vehicle prices rose much more during that period and have since come down harder, although there are reasons to think that those prices may have also hit bottom.

{kind=link}

We were supposed to have been done with this sort of inflation as consumer spending patterns normalized, retailers used discounts to get rid of excess inventories, and supply chains became unclogged. But while things improved in the second half of 2022, the process of improvement seems to have paused, if not reversed outright. That could become another potential source of upward pressure on prices (as long as nominal incomes continue to rise robustly).

The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index stopped falling back in October 2022, even if it is much closer to normal relative to its December 2021 peak. That has coincided with an unfortunate turn in input prices, according to the Producer Price Index (PPI).

"soft" - Google News

February 18, 2023 at 09:36AM

https://ift.tt/UDuSger

"Soft Landing"? More Like "No Landing" - The Overshoot

"soft" - Google News

https://ift.tt/W5vlCVJ

https://ift.tt/4QyZJou

Bagikan Berita Ini

0 Response to ""Soft Landing"? More Like "No Landing" - The Overshoot"

Post a Comment